Published Date:

Jan 3, 2024

Updated Date:

January 5, 2024

Learn about how to measure and report financed emissions aligned with guidance from Partnership for Carbon Accounting Financials (PCAF).

Financed emissions refer to indirect greenhouse gas (GHG) emissions arising from financial services, investments, and lending activities conducted by investors and financial service providers. As a practical example, banks often indirectly contribute to financed emissions by financing fossil fuel companies. Financed emissions are categorized as scope 3, category 15 under the Greenhouse Gas Protocol (GHGP).

The landscape in this space is evolving, especially with the introduction of the International Sustainability Standards Board’s (ISSB’s) IFRS S2 climate guidance and the European Union's European Sustainability Reporting Standard (ESRS). The European Financial Reporting Advisory Group’s (EFRAG) Sustainability Reporting Board (SRB) observed a misalignment between these two new standards concerning financed emissions, as the ISSB explicitly mandates reporting of financed emissions, unlike the ESRS. However, the SRB noted that financed emissions are clearly material for credit institutions, and therefore credit institutions should report on them. It's important to note that many countries and jurisdictions are actively moving towards more comprehensive regulations in this area, so we should expect to see more requirements regarding the disclosure of financed emissions in the near future.

The IFRS S2 climate standard states that “an entity that participates in one or more financial activities associated with: asset management, commercial banking, or insurance shall disclose additional information about the financed emissions associated with those activities as part of the entity’s disclosure of its Scope 3 greenhouse gas emissions” (paragraph B37). Since direct measurements for financed emissions are often unavailable, companies must rely on indirect estimations that are challenging to measure. This article will dive into the different ways these financed emissions can be measured.

While many banks have publicly committed to achieving net-zero portfolios by 2050, the practical implementation of measuring financed emissions has been undertaken by only a select few. KPMG underscores this by stating that most banks currently do not incorporate financed emissions due to challenges with data collection and the time-intensive process required for effective reporting. Thus, it is crucial for financial institutions to initiate their efforts in this space.

To ensure that the financed emission measurement requirements did not stifle the evolution of industry practices, the ISSB created high level requirements across all financial activities. The financed emissions disclosure requirements include the following for asset management, commercial banking, and insurance activities:[1]

Asset Management - the disclosure should include the following:

Commercial Banking & Insurance - the disclosure should include the following:

As mentioned before, these measurement requirements are high level, and IFRS S2 does not lay out a step-by-step process for calculating financed emissions. Instead, it only requires that companies disclose “the method of allocation the entity used to attribute its share of emissions in relation to the size of investments.” These high-level measurement requirements offer flexibility and supports industry development. However, the lack of measurement methodology creates complexity and confusion as there is not a universally accepted measuring standard. Thus, different companies use different data sources which makes consistent and transparent measurement challenging.

A significant resource for measuring financed emissions that has gained widespread attention is the Partnership for Carbon Accounting Financials (PCAF). PCAF represents an industry-driven initiative with a focused mission to promote consistent measurement and disclosure of financed emissions within the financial sector. As of November 2023, more than 440 financial institutions holding over $94.7 trillion in total assets were subscribed to the PCAF initiative. Prominent institutions such as BlackRock, Morgan Stanley, Deutsch Bank, Barclays, and Bank of America are among the prominent subscribers to the PCAF initiative, underscoring its influence and industry-wide significance.

In response to the industry's demand for a standardized approach to measure and report financed emissions, PCAF has developed The Global GHG Accounting and Reporting Standard for the Financial Industry. This Standard marries deep industry expertise with the rigorous standards of the GHG Protocol.[2] PCAF aligns with the Carbon Disclosure Project (CDP), the Science Based Targets initiative (SBTi), and the Task Force on Climate-Related Financial Disclosures (TCFD) to enhance reporting efficiency and complement the guidelines of these respective initiatives. The GHG Protocol has assessed the Standard and has confirmed its compliance with the Corporate Value Chain (Scope 3) Accounting and Reporting Standard, for Category 15 investment activities.[3]

Financed emissions are assigned to financial institutions using consistent accounting principles that are tailored to different asset classes. It should be noted that the PCAF Standard was developed primarily for use by banks and, therefore, has not yet fully addressed the asset management and portfolio context. Guidance is continually being proposed and reevaluated for various asset classes. However, within the Asset Management and Commercial Banking sectors, PCAF currently provides methodological guidance to measure and disclose GHG emissions associated with the following six asset classes:*

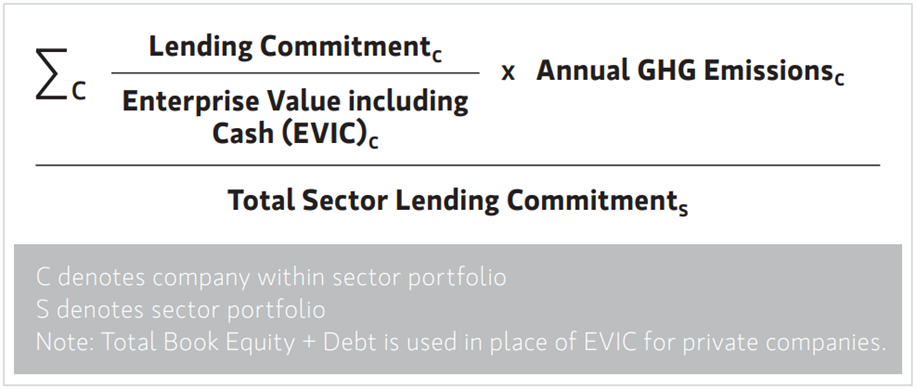

Although each of these asset classes are measured differently, PCAF consistently uses an attribution methodology to assign financed emissions for all asset classes. In general, the PCAF emissions attribution methodology is based on a straightforward concept: it calculates emissions by comparing the financial institution's investment in a company to the enterprise value of that company, which includes its debt, equity, and cash. This attribution factor is then applied to that entity’s GHG emissions. The specific calculations for each of these asset classes are depicted below[4]:

This generally straightforward allocation principle can be difficult to implement in practice. Factors like a company's ownership structure, market price fluctuations, and limited data availability can make it hard for financial institutions to calculate financed emissions. To the extent possible, companies should prioritize the use of precise and direct data. Nevertheless, in cases where direct data is unavailable, estimations may be calculated with activity and sector-level data, along with emissions proxy factors.

Although the scarcity of data presents challenges in calculating financed emissions, the PCAF Standard mitigates this issue by offering guidance on data quality scoring for each segment. The PCAF Standard highlights the quality of the data used so investors are more informed. Emissions reported directly by companies often receive favorable data quality scores because of their specificity and the potential for third-party verification. Conversely, emissions factors based on economic activity are typically considered to have lower data quality, resulting in less favorable scores. These scoring metrics are reported alongside financed emissions and allow reviewers to understand the accuracy of the related financed emission measurements.

The following examples of disclosures by BlackRock and Morgan Stanley can be found on PCAF's website. PCAF provides these disclosures from its signatories on their website to enhance stakeholder transparency. It is important to note that the incorporation of these disclosures on the website does not imply certification or endorsement by PCAF regarding the alignment level of a disclosure with the PCAF Standard. Nevertheless, considering the novelty of these standards and disclosures, they serve as valuable examples for gaining insight into how companies approach the disclosure of financed emissions in practice.

PCAF has also developed a methodology for insurance companies to report financed emissions. The guidance provides insured-emissions calculation methods for commercial lines and personal motor insurance. Much like PCAF's guidance on financial financed emissions, its insurance methodology also relies on attribution factors to calculate the insurer's total financed emissions. Emissions linked to insurance will be computed by multiplying a specific attribution factor by the emissions generated by an insured company.

PCAF’s guidance outlines distinct attribution factors for commercial lines and personal motor portfolios. In the case of commercial lines, the attribution factor is derived from the insurance premium in relation to the customer's revenue. For personal motor portfolios, the attribution factor is based on the insurer's revenue from the insured (insurance premium) in relation to the annual expenses associated with vehicle ownership. Please see the toggles below to view the specific formulas for these calculations.[8]

Data quality is also assessed, scored, and reported for insurance-associated emissions just as it is for financed emissions. These scoring metrics are reported alongside financed emissions and allow reviewers to understand the accuracy of the related financed emission measurements.

Financed emissions reporting is experiencing a transformative shift, marked by evolving standards and regulatory frameworks. The introduction of IFRS S2 and ESRS evidences the importance of measuring and disclosing financed emissions. As these standards gain prominence, a comprehensive regulatory framework becomes imminent. Measuring financed emissions presents challenges, including data complexities and a lack of universal standards, necessitating a more concerted effort from financial institutions. The Partnership for Carbon Accounting Financials (PCAF) has emerged as a key resource, guiding financial institutions toward consistent measurement practices. Its Global GHG Accounting and Reporting Standard reflects a collaborative, credible approach. The journey toward a sustainable financial future hinges on a collective dedication to innovative standardized approaches. As methodologies mature and industry practices evolve, accurate and meaningful reporting remains central to addressing climate-related risks and fostering a low-carbon economy.