Published:

Apr 22, 2024

Updated:

April 24, 2024

This articles discusses the impact of California’s Climate Corporate Data Accountability Act (CCDAA), or SB 253. Effective 2026, this law mandates standardized greenhouse gas reporting for companies with $1B+ revenue. Explore how this legislation sets a new standard for corporate transparency in combating climate change.

On October 7, 2023, California Governor, Gavin Newsom, signed two bills related to ESG reporting. This article focuses on the Climate Corporate Data Accountability Act (CCDAA), which mandates updated requirements for greenhouse gas reporting from the State Air Resources Board. For more information on the other bill, the Climate-Related Financial Risk Act (CRFRA), see our article here.

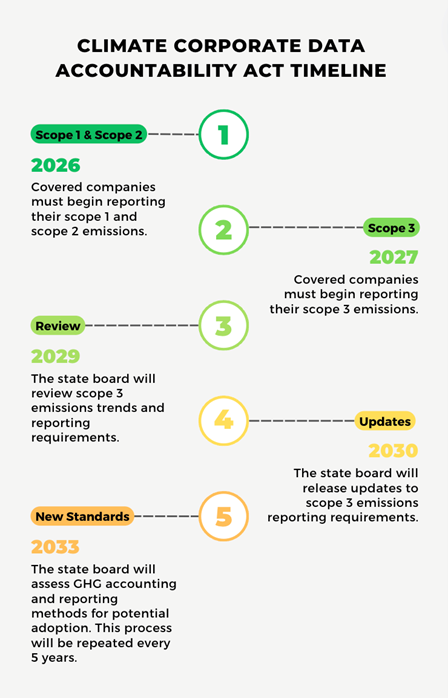

The CCDAA sets ESG reporting standards that affect all entities operating in California with annual revenue in excess of $1B in the previous fiscal year. For covered companies, scope 1, 2, and 3 greenhouse gas emissions must be reported according to Greenhouse Gas Protocol standards. For more information on Greenhouse Gas Protocol see our other article.

Emissions data will be filed with the state board, who will contract an academic institution (university or laboratory) to aggregate and analyze the data. Individual company data and aggregate data will be publicly available through the state’s digital platform.

What are scope 1, scope 2, and scope 3 emissions? According to the CCDAA, these classifications are defined as:

While each classification of emissions will require additional measurement practices, scope 3 emissions will require the most time and capital to track. The extra year of preparation (2026 for scope 1 and scope 2 vs 2027 for scope 3) will allow companies to prepare for these detailed reporting requirements.

Since this bill was signed, the SEC has adopted new ESG disclosure rules. These rules do not require scope 3 emissions reporting. While the state board reserves the right to adopt new standards, the CCDAA specifies that the new standards must require scope 1, scope 2, and scope 3 reporting. This requirement eliminates the option for companies to use SEC rules for compliance with the CCDAA.

Emissions data must be audited by an independent third-party. From 2026-2030, scope 1 and scope 2 emissions should be audited at the limited assurance level. Beginning in 2030, scope 1 and scope 2 emissions need to be audited at a reasonable assurance level. While scope 3 emissions must be disclosed beginning in 2027, there is no assurance requirement until 2030, when a limited assurance level should be performed.

Scope 3 emissions disclosures made with “reasonable basis and disclosed in good faith” will not be subject to penalties. The only penalties for scope 3 disclosures between 2027 and 2030 will be assessed for parties who neglect to file required disclosures.

Assurance providers should have “significant experience in measuring, analyzing, reporting, or attesting to the emission of greenhouse gasses and sufficient competence and capabilities necessary to perform engagements in accordance with professional standards and applicable legal and regulatory requirements.”

The Climate Corporate Data Accountability Act represents a significant step forward in regulating greenhouse gas emissions reporting for large entities operating in California. With its structured approach, the CCDAA mandates reporting of scope 1, scope 2, and scope 3 emissions, ensuring comprehensive transparency in environmental impact assessment. By setting rigorous standards, the CCDAA underscores California's commitment to addressing climate change and promoting sustainable business practices. While these reporting requirements appease many environmentalists, many corporate executives are concerned about the cost and time required to comply with the CCDAA. It is likely that companies will consider various tactics to circumvent or delay compliance, such as legal challenges to the legislation, lobbying efforts to influence amendments or exemptions, or even shifting operations. As legislation evolves and adapts to changing environmental and economic landscapes, it will continue to play a pivotal role in shaping corporate responsibility and environmental stewardship.