Published Date:

Dec 6, 2023

Updated Date:

December 7, 2023

Learn about the CDSB framework and application guides and understand their role in the evolving landscape of ESG reporting.

The Climate Disclosure Standards Board (CDSB) is an “international consortium of business and environmental non-governmental organizations….committed to advancing and aligning the global mainstream corporate reporting model to equate natural capital with financial capital.” Established in 2007, the CDSB was one of the first groups to create climate-related disclosure standards. In 2010, they released the “Framework for reporting climate information,” followed by specific application guides for biodiversity and water in 2021. The CDSB framework was listed as a method of compliance in the UK Companies Act and won awards for its advocacy of sustainable reporting measures. In 2022, “the CDSB was consolidated into the IFRS Foundation to support the work of the newly established International Sustainability Standards Board (ISSB),”1 which has since released additional standards on sustainability disclosures. For an overview of these standards, see our article on ISSB Standards.

Although no independent work is now being done by the CDSB, its framework and resources continue to serve as valuable guides for companies looking to improve their sustainability disclosures. In fact, the new ISSB standard, IFRS S1, still cites the CDSB guides as a source of data in the reporting process. Because these frameworks are still relevant, this article will provide a brief overview of the CDSB frameworks and how companies can use them in today’s environment.

While many iterations and updates were made to the frameworks since the initial release in 2010, there now exists one overall framework with three application guides for certain reporting topics. The first, issued in 2020, was the “Application guidance for climate-related disclosures,” followed by the “Application guidance for water-related disclosures” and the “Application guidance for biodiversity-related disclosures” in 2021. These three frameworks are designed to help companies report on the climate, water, and biodiversity-related issues relevant to business today. This section will first explore the overall framework and then discuss the application guides.

The CDSB Framework establishes a method for reporting environmental & social information, which includes information about natural dependencies, the environmental and social impact of activities, risks and opportunities, policies and strategies, and target performance. Its objective is to help companies standardize their environmental reporting for the benefit of investors.

The framework is divided into two main components: guiding principles and reporting requirements. There are seven guiding principles that serve as broad guidelines for the quality of disclosures. Additionally, there are twelve reporting requirements that pinpoint specific areas where disclosures are necessary in the financial statements. Below is a table outlining these principles and requirements.2

The core of the three application guides lies in providing detailed insight into the first six reporting requirements from the CDSB Framework: governance, environmental policies, risks and opportunities, sources of environmental impact, performance and comparative analysis, and outlook. Each requirement is accompanied by a checklist for making effective disclosures, detailed reporting suggestions, a selection of further useful resources, and examples of good practice. The guides also cover topics such as the structure of guidance, reporting boundaries, materiality considerations, mainstream reporting, and the basis for conclusions.

The climate-related disclosure guide spans 19 pages,3 while the water-related guide comprises 59 pages,4 and the biodiversity guide extends to 95 pages.5 The extended length of the latter guides may come from the limited availability of established standards in these areas. While many frameworks and standards address climate-related disclosures, very few are directed toward water or biodiversity, necessitating more comprehensive coverage by the CDSB. However, regardless of length, all three application guides offer a helpful and easy-to-understand overview of effective ways to report sustainability-related information. The inclusion of numerous linked resources and real-life examples makes the guides an excellent source for companies venturing into ESG reporting.

As the market’s demand for companies to disclose their sustainability practices has increased, various frameworks and standards have emerged to help companies accomplish this goal. The question now is: how does the CDSB Framework fit in with these other standards?

One of the leading ESG frameworks is from the Task Force on Climate-Related Financial Disclosures (TCFD). The CDSB has continuously strived to align itself with the TCFD by supporting initiatives and updating the frameworks to reflect TCFD recommendations. As per the CDSB website, the CDSB “provides companies and policymakers with the practical tools and technical expertise they need to implement the recommendations of the TCFD.”1

To accomplish this collaboration with the TCFD, all three application guides include an appendix that maps the CDSB reporting requirements to the TCFD recommendations. For more information about what these TCFD recommendations are, please visit our TCFD article here. (link forthcoming)

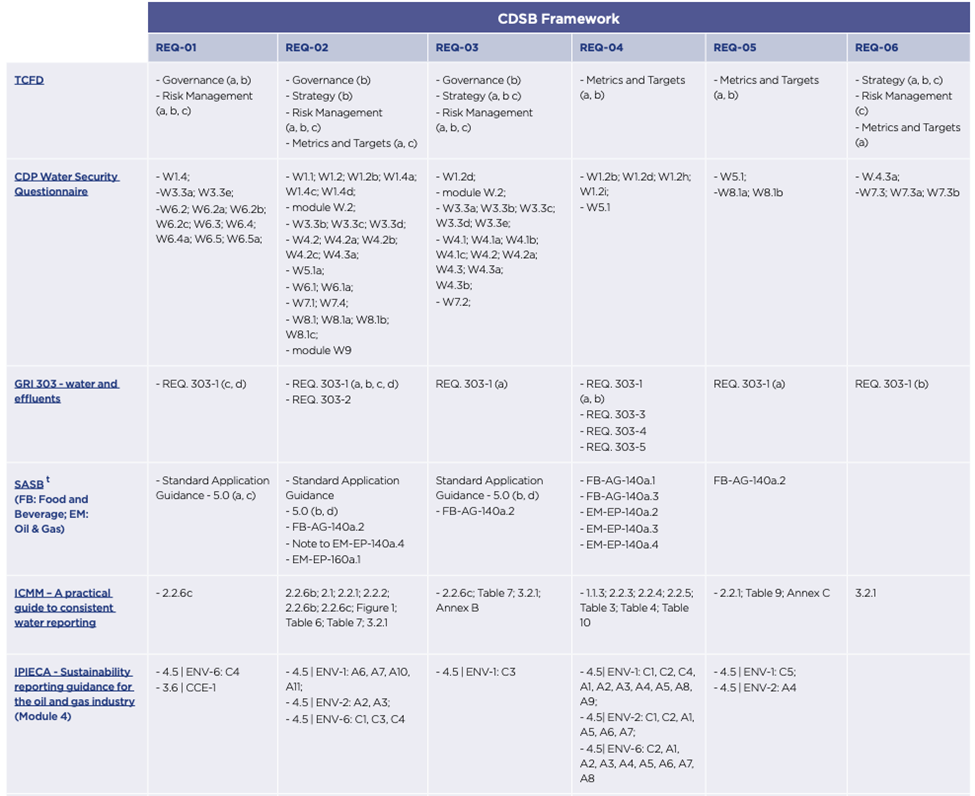

In the water and biodiversity guides, the appendix also includes a mapping of the CDSB framework requirements to other frameworks such as CDP, GRI, SASB, ICMM, and IPIECA. These matrices assist companies in understanding how the CDSB framework aligns with other frameworks they currently use or may consider adopting. An example of this matrix is found below.4

Perhaps the most direct connection to another standard is found in the International Sustainability Standards Board’s release of International Financial Reporting Standard S1: General Requirements for Disclosure of Sustainability-Related Financial Information. Under this standard, companies are required to disclose their sustainability-related risks and opportunities. To identify this information, “an entity may refer to and consider the applicability of: the CDSB Framework Application Guidance for Water-related Disclosures and the CDSB Framework Application Guidance for Biodiversity-related Disclosures.”6 In fact, the consideration of CDSB guides was originally mandatory, but was later made optional to facilitate easier implementation.7 For more insights into the identification process, please visit our article here.

IFRS S1 stands as the leading international standard for companies. Consequently, many organizations will begin implementing its guidance, which includes consulting the CDSB application guides to identify and disclose sustainability risks and opportunities effectively.

Until recently, the CDSB Framework and application guides held a prominent position among ESG reporting frameworks. Before the release of anything by the TCFD or IFRS, the CDSB helped companies begin the process of reporting on environmental impacts. By 2017, 374 companies across 32 countries and 10 sectors were utilizing the CDSB framework to guide their reporting needs.1

Today, new standards have been released, such as those described above. As stated on the CDSB website, the CDSB framework and application guides can be used to support the TCFD and IFRS standards until even more concrete guidance is released. Companies can continue to leverage the detailed, practical insights offered by the CDSB to enhance their sustainability reporting.